Goods, Services, and Consumers

Economic products are goods or services that are useful,

relatively scarce, and transferable.

Economics is concerned with economic productsgoods and

services that are useful, relatively scarce, and transferable to others.

Economic products help us satisfy our wants and needs. Because they

are both scarce and useful, they command a price.

Goods

There are different types of economic products.

The first one is a gooda useful, tangible item, such as a book,

car, or compact disc player, that satisfies a want. When manufactured

goods are used to produce other goods and services, they are called capital

goods. An example of a capital good would be a robot welder in a

factory, an oven in a bakery, or a computer in a high school. Goods

intended for final use by individuals are consumer goods.

good

tangible economic product that is useful, relatively

scarce, and transferable to others

consumer good

good intended for final use by consumers rather than

businesses

Any good that lasts three years or more when used on a

regular basis is called a durable good. Durable goods include

both capital goods, such as robot welders, and consumer goods, such as

automobiles. A nondurable good is an item that lasts for fewer

than three years when used on a regular basis. Food, writing paper,

and most clothing items are examples of nondurable goods.

durable good

a good that lasts for at least three years when used

regularly

nondurable good

a good that wears out or lasts for fewer than three

years when used regularly

Services

The other type of economic product is a service,

or work that is performed for someone. Services include haircuts,

home repairs, and forms of entertainment such as concerts. They also

include the work that doctors, lawyers, and teachers perform. The

difference between a good and a service is that a good is tangible, or

something that can be touched, while a service is not.

service

work or labor performed for someone

Consumers

Consumers are the people who use goods and services to

satisfy their wants and needs. As consumers, people indulge in consumption,

the process of using up goods and services in order to satisfy wants and

needs.

How are goods, services, and

consumers related?

REVIEW & DO

NOW

Answer the following questions: |

| What is a good?

What is a consumer good? |

|

| What is the difference between a durable good

and a nondurable good?

What is a service? |

|

|

|

Value, Utility, and Wealth

The value of a good or service depends on its scarcity

and utility.

In economics, value refers to a worth that can be expressed

in dollars and cents. Why, then, does something have value, and why

are some things more valuable than others? To answer these questions, it

helps to review a problem Adam Smith, a Scottish social philosopher, faced

back in 1776.

The Paradox of Value

Adam Smith was one of the first people to describe how

markets work. He observed that some necessities, such as water, had

a very low monetary value. On the other hand, some non-necessities,

such as diamonds, had a very high value. Smith called this contradiction

the paradox of value. Economists knew that scarcity was necessary

for something to have value. Still, scarcity by itself could not

fully explain how value is determined.

paradox of value

apparent contradiction between the high monetary value

of a nonessential item and the low value of an essential item

Utility

It turned out that for something to have value, it must

also have utility, or the capacity to be useful and provide satisfaction.

Utility is not something that is fixed or even measurable, like weight

or height. Instead, the utility of a good or service may vary from

one person to the next. One person may get a great deal of satisfaction

from a home computer; another may get very little. One person may

enjoy a rock concert; another may not.

utility

ability or capacity of a good or service to be useful

and give satisfaction to someone

Value

For something to have monetary value, economists decided,

it must be scarce and have utility. This is the solution to the paradox

of value. Diamonds are scarce and have utility, thus they possess

a value that can be stated in monetary terms. Water has utility but

is not scarce enough in most places to give it much value. Therefore,

water is less expensive, or has less monetary value, than diamonds.

The emphasis on monetary value is important to economists.

Unlike moral or social value, which is the topic of other social sciences,

the value of something in terms of dollars and cents is a concept that

everyone can easily understand.

value

monetary worth of a good or service as determined

by the market

Wealth

In an economic sense, the accumulation of products that

are tangible, scarce, useful, and transferable from one person to another

is wealth. A nations wealth is comprised of all tangible

itemsincluding natural resources, factories, stores, houses, motels, theaters,

furniture, clothing, books, highways, video games, and even basketballsthat

can be exchanged.

While goods are counted as wealth, services are not, because

they are intangible. However, this does not mean that services are

not useful or valuable. Indeed, when Adam Smith published his famous

book The Wealth of Nations in 1776, he was referring specifically to the

abilities and skills of a nations people as the source of its wealth.

For Smith, if a countrys material possessions were taken away, its people,

through their efforts and skills, could restore these possessions.

On the other hand, if a countrys people were taken away, its wealth would

deteriorate.

wealth

sum of tangible economic goods that are scarce, useful,

and transferable from one person to another

How are value and utility related?

REVIEW & DO

NOW

Answer the following questions: |

| What is the paradox of value?

What is utility? |

|

| What is meant by value?

What is wealth? |

|

|

|

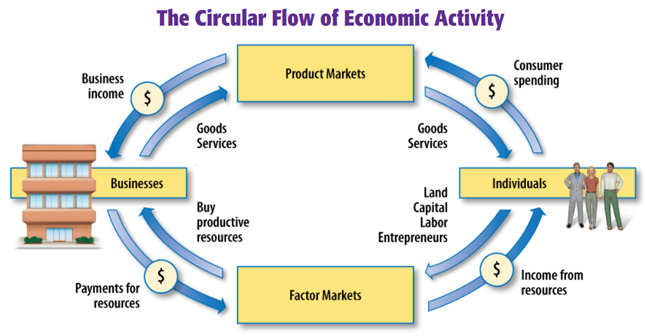

The Circular Flow of Economic Activity

The economic activity in markets connects individuals

and businesses.

The wealth that an economy generates is made possible

by the circular flow of economic activity. The key feature of this

circular flow is the market, a location or other mechanism that

allows buyers and sellers to exchange a specific product. Markets

may be local, national, or globaland they can even exist in cyberspace.

market

meeting place or mechanism that allows buyers and

sellers to come together

Factor Markets

As shown in Figure 1.3, individuals earn their incomes

in factor markets, where the factors of production are bought and

sold.

This is where entrepreneurs hire labor for wages and salaries,

acquire land in return for rent, and borrow money. The concept of

a factor market is a simplified but realistic version of the real world.

For example, you participate in the factor market when you work and sell

your labor to an employer.

factor market

market where the factors of production are bought

and sold

Product Markets

After individuals receive their income from the resources

they sell in a factor market, they spend it in product markets.

These are markets where producers sell their goods and services.

Thus, the wages and salaries that individuals receive from businesses in

the factor markets returns to businesses in the product markets.

Businesses then use this money to produce more goods and services, and

the cycle of economic activity repeats itself.

product market

market where goods and services are bought and sold

What roles do factor markets

and product markets play in the economy?

REVIEW & DO

NOW

Answer the following questions: |

| What is a market?

What is a factor market? |

|

| What is a product market? |

|

|

|

Productivity and Economic Growth

A nations economic growth is due to several factors.

Economic growth occurs when a nations total output

of goods and services increases over time. This means that the circular

flow becomes larger, with more factors of production, goods, and services

flowing in one direction and more payments in the opposite direction.

Productivity is the most important factor contributing to economic growth.

economic growth

increase in a nations total output of goods and services

over time

Productivity

Everyone in a society benefits when scarce resources are

used efficiently. This is described by the term productivity,

a measure of the amount of goods and services produced with a given amount

of resources in a specific period of time.

Productivity goes up whenever more can be produced with

the same amount of resources. For example, if a company produced

5,000 pencils in an hour, and it produced 5,100 in the next hour with the

same amount of labor and capital, productivity went up. Productivity

is often discussed in terms of labor, but it applies to all factors of

production.

productivity

measure of the amount of output produced with a given

amount of productive factors

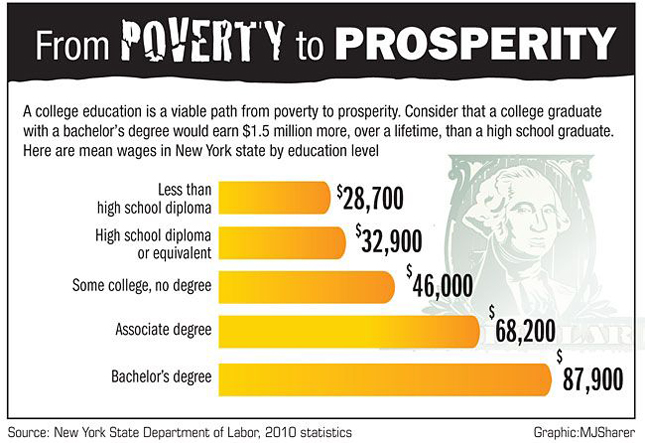

Investing in Human Capital

A major contribution to productivity comes from investments

in human capital, the sum of peoples skills, abilities, health,

knowledge, and motivation. Government can invest in human capital

by providing education and health care. Businesses can invest in

training and other programs that improve the skills of their workers.

Individuals can invest in their own education by completing

high school, going to technical school, or attending college. The

chart below shows that investments in education can have substantial payoffs.

According to the table, high school graduates earn substantially more than

nongraduates, and college graduates make even more than high school graduates.

Educational investments require that we make a sacrifice today so we can

have a better life in the future, and few investments generate higher returns.

human capital

sum of peoples skills, abilities, health, knowledge

and motivation

Division of Labor and Specialization

Division of labor and specialization can improve productivity.

Division of labor is a way of organizing work so that each individual

worker completes a separate part of the work. In most cases, a worker

who performs a few tasks many times a day is likely to be more proficient

than a worker who performs hundreds of different tasks in the same period.

Specialization takes place when factors of production

perform only tasks they can do better or more efficiently than others.

The division of labor makes specialization possible. For example,

the assembly of a product may be broken down into a number of separate

tasks (the division of labor). Then each worker can perform the specific

task he or she does best (specialization).

One example of the advantages offered by the division

of labor and specialization is Henry Fords use of the assembly line in

automobile manufacturing. Having each worker add one part to the

car, rather than a few workers assembling the entire vehicle, cut the assembly

time of a car from a day and a half to just over 90 minutesand reduced

the price of a new car by more than 50 percent.

division of labor

division of work into a number of separate tasks to

be performed by different workers

specialization

assignment of tasks to the workers, factories, regions,

or nations that can perform them more efficiently

Economic Interdependence

The U.S. economy has a remarkable degree of economic

interdependence. This means that we rely on others, and others

rely on us, to provide most of the goods and services we consume.

As a result, events in one part of the world often have a dramatic impact

elsewhere.

This does not mean that interdependence is necessarily

bad. The gains in productivity and income that result from specialization

almost always offset the costs associated with the loss of self-sufficiency.

economic interdependence

mutual dependency of one persons, firms, or regions

economic activities on anothers

What role does specialization

play in the productivity of an economy?

REVIEW & DO

NOW

Answer the following questions: |

| What is meant by economic growth?

What is productivity?

What is human capital? |

|

| What is division of labor?

What is specialization?

What is economic interdependence? |

|

|

|

|