Trade-Offs and Opportunity Cost

Economic choices involve trade-offs and the careful

evaluation of opportunity costs.

There are alternatives and costs to everything we do.

In a world where there is no such thing as a free lunch, it pays to examine

these concepts closely.

Trade-Offs

Every decision we make has its trade-offs, or alternative

choices. One way to help us make decisions is to construct models

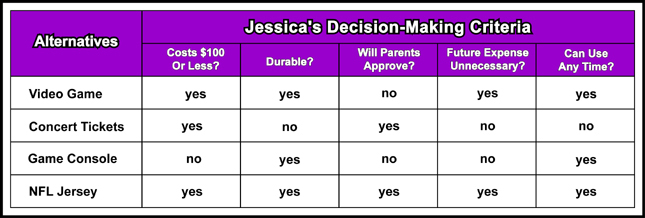

such as the grid shown below. This grid shows how Jessica decides

to spend a $100 gift.

trade-off

alternative that is available whenever a choice is

to be made

Jessica likes several alternatives: a video game, concert

tickets, a game console, and a replica NFL jersey. At the same time,

she realizes that each item has advantages and disadvantages. Some

of the items can be used more than once, and some might require her parents

consent. Some might even require her to kick in a little extra money.

To help with her decision, Jessica can draw a grid that

lists her alternatives and several criteria by which to judge them.

Then she evaluates each alternative with a yes or no. In the end, Jessica

chooses the jersey because it satisfies more of her criteria than any other

alternative. Plus, she had money left over.

Using a decision-making grid is one way to analyze an

economic problem. It forces you to consider a number of alternatives

and the criteria youll use to evaluate the alternatives. Finally,

it makes you evaluate each alternative based on the criteria you selected.

Opportunity Cost

People often think of cost in terms of dollars and cents.

To an economist, however, cost means more than the price tag on a good

or service. Instead, economists think broadly in terms of opportunity

cost, the cost of the next-best alternative. When Jessica decided

to purchase the jersey, her opportunity cost was the video gamethe next

best choice she gave up. In contrast, trade-offs are all of the other

alternatives that she could have chosen.

Even time has an opportunity cost, although you cannot

always put a monetary value on it. The opportunity cost of reading

this economics website, for example, the history paper or math homework

that you could not do at the same time.

How are trade-offs and opportunity

cost related?

REVIEW & DO

NOW

Answer the following questions: |

|

|

| What is meant by opportunity cost? |

|

|

|

Production Possibilities

Economies face trade-offs when deciding what goods

and services to produce.

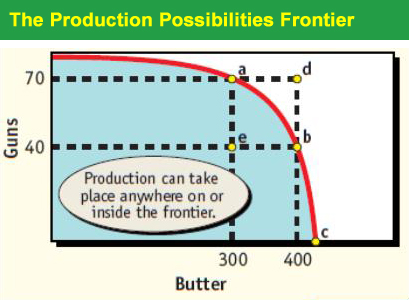

| To illustrate opportunity cost, economists use the production

possibilities frontier, a diagram representing various combinations

of goods and services an economy can produce when all its resources are

in use. In the example on the right, a mythical mega-corporation

called the Alpha Corporation produces two goods for the countryguns and

butter. |

|

|

production possibilities frontier diagram

representing the maximum combinations of goods and/or

services an economy can produce when all productive resources are fully

employed

Identifying Possible Alternatives

Even though Alpha produces only two goods, the country

has a number of

alternatives available to it. For example, it could

choose to use all of its resources to produce 70 units of guns and 300

units of butter, which is shown as point a in the Production Possibilities

Frontier diagram. Or it could shift some of its resources out of

gun production and into butter, thereby moving to point b.

Alpha could even choose to produce at point c, which represents

all butter and no guns, or at point e, which is inside the frontier.

Alpha has many alternatives available to it, which is

why the figure is called a production possibilities frontier. Eventually,

though, Alpha will have to settle on a single combination such as point

a,

b, or any other point on or inside the curve, because its resources

are limited.

Fully Employed Resources

All points on the curve such as a, b, and

c

represent maximum combinations of output that are possible if all resources

are fully employed. To illustrate, suppose that Alpha is producing

at point a, and the people would like to move to point d,

which represents the same amount of guns, but more butter. As long

as all resources are fully employed at point a, there are no extra

resources available to produce the extra butter. Therefore,

point

d cannot be reached, nor can any other point outside the curve.

This is why the figure is called a production possibilities frontierto

indicate the maximum combinations of goods and services that can be produced.

The Cost of Idle Resources

If some resources were not fully employed, then it would

be impossible for the Alpha Corporation to reach its maximum potential

production. Suppose that Alpha was producing at point b when

workers in the butter industry went on strike. Butter production

would fall, causing total output to change to point e. The

opportunity cost of the unemployed resources would be the 100 units of

lost butter production.

Production at point e could also be the result

of other idle resources, such as factories or land that are available but

not being used. As long as some resources are idle, the corporation

cannot produce on its frontierwhich is another way of saying that it cannot

reach its full production potential.

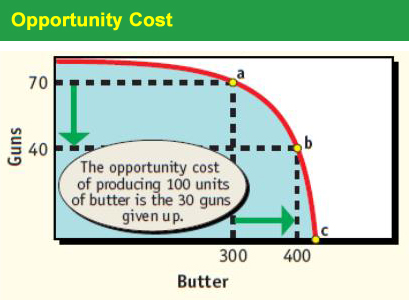

Opportunity Cost

| Suppose that the Alpha Corporation was producing at point

a and that it wanted to move to point b. This is clearly

possible as long as point b is not outside the production possibilities

frontier. However, Alpha will have to give something up in return.

As shown on the right, the opportunity cost of producing the 100 additional

units of butter is the 30 units of guns given up. |

|

|

As you can see, opportunity cost applies to almost

all activities, and it is not always measured in terms of dollars and cents.

For example, you need to balance the time you spend doing homework and

the time you spend with your friends. If you decide to spend extra

hours on your homework, the opportunity cost of this action is the time

that you cannot spend with your friends. You normally have a number

of trade-offs available whenever you make a decision, and the opportunity

cost of the choice you make is the value of the next best alternative that

you give up.

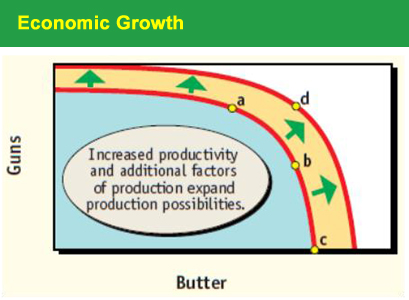

Economic Growth

The production possibilities frontier represents potential

output at a given point in time. Eventually, however, changes may

cause the production possibilities frontier to expand. The population

may grow, the stock of capital may expand, technology may improve, or productivity

may increase. If any of these changes occur, then the Alpha Corporation

will be able to produce more in the future.

| The effect of economic growth in the economy or in industry

is shown in the diagram on the right. Economic growth, made possible

by having more resources, better technology, or increased productivity,

causes the production possibilities frontier to move outward. Economic

growth will eventually allow the Alpha Corporation to produce both guns

and butter at point d, which it could not do earlier. |

|

|

How can the production possibilities

frontier be used to illustrate economic growth?

REVIEW & DO

NOW

Answer the following questions: |

| What is a production possibilities frontier diagram? |

|

|

|

|

Thinking Like an Economist

Economists use a strategy called cost-benefit analysis

to evaluate choices.

Because economists study how people satisfy seemingly

unlimited and competing wants through the careful use of scarce resources,

they are concerned with strategies that will help people make the best

choices. Two strategies are building models and preparing a cost-benefit

analysis.

Build Simple Models

One of the most important strategies is to build economic

models. An economic model is a simplified equation, graph,

or figure showing how something works. Simple models can often reduce

complex situations to their most basic elements. To illustrate, the

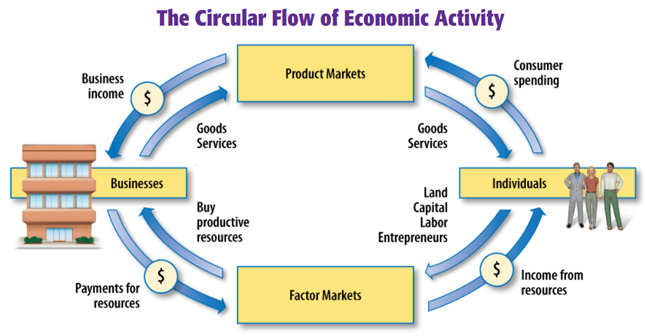

production possibility frontiers in this section and the circular flow

diagram below are examples of how complex economic activity can be explained

by a simple model.

economic model

simplified version of a complex concept or behavior

expressed in the form of an equation, graph, or illustration

.

| Another basic model is the production possibilities frontier

shown on the right. Realistically, of course, economies are able

to produce more than two goods or services, but the concepts of trade-offs

and opportunity costs are easier to illustrate if only two products are

examined. As a result, simple models such as these are sometimes

all that economists need to analyze or describe an actual situation. |

|

|

It is important to realize that models are based on assumptions,

or things we think are true. In general, the quality of a model is

no better than the assumptions on which it is based, but a model with simple

assumptions is usually easier to understand. In the case of the production

possibilities frontier, for example, we assumed that only two goods could

be produced. This made the model easier to illustrate and still allowed

us to discuss the concepts of trade-offs and opportunity costs.

It is also important to keep in mind that models can be

revised to make them better. If an economic model helps us to make

a prediction that turns out to be right, the model can be used again.

If the prediction is wrong, the model might be changed to make better predictions

the next time.

Apply Cost-Benefit Analysis

Most economic decisions can be evaluated with cost-benefit

analysis, a way of comparing the costs of an action to the benefits

received. This is what Jesse did when he devised a decision-making

grid. This decision can be made subjectively, as when Jesse selected

the jersey, or it can be made more objectively, especially if the costs

of the various alternatives are different.

cost-benefit

analysis way of thinking about a choice that compares

the cost of an action to its benefits

To illustrate, suppose that you have to make a decision,

and you like choices A and B equally. If B costs less, it would be

the better choice because you would get more satisfaction per dollar spent.

Businesses make investment decisions in exactly this manner, choosing to

invest in projects that give the highest return per dollar spent or, in

other words, the best cost-benefit ratio.

Take Small, Incremental Steps

Finally, it also helps to take small, incremental steps

toward the final goal. This is especially valuable when we are unsure

of the exact cost involved. If the cost turns out to be larger than

we anticipated, then the resulting decision can be reversed without too

much being lost.

How does cost-benefit analysis

help make economic decisions?

REVIEW & DO

NOW

Answer the following questions: |

| What are economic models? |

|

| What is a cost-benefit analysis? |

|

|

|

The Road Ahead

The study of economics helps people become better

citizens.

The study of economics does more than explain how people

deal with scarcity. Economics also includes the study of how things

are made, bought, sold, and used. It provides insight as to how incomes

are earned and spent, how jobs are created, and how the economy works on

a daily basis. The study of economics also gives us a better understanding

of the workings of a free enterprise economyone in which consumers

and privately owned businesses, rather than the government, make the majority

of the WHAT, HOW, and FOR WHOM decisions.

free enterprise economy

economy market economy in which privately owned businesses

have the freedom to operate for a profit with limited government intervention

Topics and Issues

The study of economics will provide you with a working

knowledge of the economic incentives, laws of supply and demand, price

system, economic institutions, and property rights that make the U.S.

economy function. Along the way, you will learn about topics such

as unemployment, the business cycle, inflation, and economic growth.

You will also examine the role of business, labor, and government in the

U.S. economy, as well as the relationship of the United States economy

with the international community.

All of these topics have a bearing on our standard

of livingthe quality of life based on the ownership of the necessities

and luxuries that make life easier. As you study economics, you will

learn how to measure the value of our production and how productivity helps

determine our standard of living. You will find, however, that the

way the American people make economic decisions is not the only way to

make these decisions.

standard of living

quality of life based on ownership of necessities

and luxuries that make life easier

Economists have identified three basic kinds of economic

systems. We will analyze these systems and how their organization

affects decision making in the next chapter.

Economics for Citizenship

The study of economics helps us become better decision

makersin our personal lives as well as in the voting booths. Economic

issues are often debated during political campaigns, so we need to understand

the issues before deciding which candidate to support.

Most of todays political problems have important economic

aspects. For example, is it important to balance the federal budget?

How can we best keep inflation in check? What methods can we use to strengthen

our economy? The study of economics will not provide you with clear-cut

answers to all of these questions, but it will give you a better understanding

of the issues involved.

Understanding the World Around

Us

The study of economics helps us understand the complex

world around us. This is particularly useful because the world is

not as orderly as your economics textbook, for example. Your book

is neatly divided into sections for study. In contrast, society is

dynamic, and technology and other innovations always lead to changes.

Economics provides a framework for analysisa structure

that helps explain how things are organized. Because this framework

describes the incentives that influence behavior, it helps us understand

why and how the world changes.

In practice, the world of economics is complex and the

road ahead is bumpy. As we study economics, however, we will gain

a much better appreciation of how we affect the world and how it affects

us.

How do you think our society

would be different if citizens did not study economics?

REVIEW & DO

NOW

Answer the following questions: |

| What is a free market economy? |

|

| What is meant by standard of living? |

|

|

|

|